Global financial markets are keenly interested in China's short-term economic direction and policy choices. American policy should look farther. If China chooses to try to stimulate its economy in the second half of the year, even if successful, it will only exacerbate a more pressing long-term challenge.

This challenge in part takes the form of too much money. While attention is focused on when the People's Republic of China (PRC) might catch the U.S. in terms of GDP, it has already passed the U.S. on some measures of its monetary base. Such high liquidity typically precedes periods of stagnation or even outright economic contraction. It is one of the surer reasons for anticipating that China's true economic growth might slow sharply, a possibility that has clear implications for American policy.

Moreover, excess Chinese liquidity has already had an impact in the U.S. The two economies are linked by Beijing's chosen balance-of-payments rules, which tie the yuan to the dollar and compel the PRC to hold excess reserves in American bonds. The U.S. has its own money supply management challenges, and communication between the two countries' monetary authorities will be valuable.

Not for All the Money in China

There are many different ways to measure the supply of money. There are also pronounced differences in national monetary systems, which cause natural differences among economies. For a large economy, the PRC is immature financially, so that more capital stays within the banking system. This is a well-recognized long-term problem.

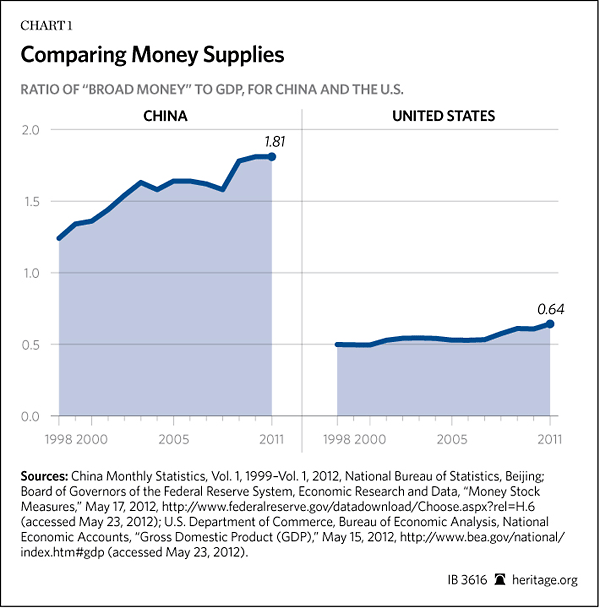

One manifestation of the problem is a comparatively high ratio of broad money M2 (currency in circulation plus demand and time deposits) to GDP. China is well above the global average on this measure, while a somewhat similar economy in Brazil is well below. Nearly all of the countries that have higher M2/GDP ratios than China are in Europe, which, in light of recent developments, is not reassuring.

More importantly, the ratio for the PRC is not only high but has been rising steadily. Since the financial crisis, a number of countries have rising liquidity, including the U.S. However, those countries with both high and clearly rising liquidity (Spain, for example) are a small and unhealthy bunch. This is not good company for China to be keeping.

The U.S. is only one point of comparison, but it is an instructive one. In 1998, China's M2was 70 percent smaller than America's. In 2011, it was 40 percent larger. While Chinese GDP expanded greatly in that period, it was still only half of American GDP at the end of last year. Yet the PRC had $3.8 trillion more in broad money supply sloshing around.

Measurements of leveraging show roughly similar problems. China's dependence on bank loans for financing intensified with the lending explosion in 2009. In 1998, loan volume was 102 percent of GDP. By 2008, it had only inched higher to 106 percent of GDP. Just three years later, though, it had jumped to 123 percent of GDP. More comprehensive measures of credit show still higher figures and steeper climbs.

What Happens Next?

There is plenty of discussion at present about short-term weakness in the Chinese economy and whether additional stimulus is the right response. The longer term is clear: On its present policy path, the effective stimulus Beijing can apply through monetary policy will continue to decline.

At the high levels of liquidity that have now been reached, further leveraging has and will continue to become increasingly ineffective. More and more money must be employed to get the same results. Barring a major policy misstep, there is no true crisis imminent. However, a crisis must loom as a possibility at some point.

This leaves Beijing with unpleasant choices. More monetary stimulus will have only a limited impact now at the cost of digging deeper into a hole that China must eventually climb out of. Whether or not further short-term stimulus is chosen, the PRC must eventually de-leverage to some extent. This will exert downward pressure on growth for some time. After years where growth has been inflated by a flood of new money, this signifies instability, and the Communist Party does not like instability.

How liquidity is drained, however, could matter a great deal. Broad money should at least stabilize relative to GDP, and total credit should slow relative to GDP. It would be greatly preferable if, at the same time, bank lending were to become less important. This could occur with financial reform. The PRC should have more commercialized banks that are more circumspect about lending under the wrong conditions. It should have more financial options so that banking is less important relative to bonds, stocks, futures, and other financial outlets.

Financial reform is not only painful; it takes time. Interest rate liberalization, de-control of financial markets (with attendant risk), and partial privatization in banking cannot be done overnight. Beijing has a bit of time, since there is no impending crisis, but genuine reform should start as soon as possible. If it begins quickly, the payoff from reform can more than offset the discomfort from the inevitable deleveraging. The PRC's financial system can shift from a source of instability to a source of efficiency.

American Involvement

Like it or not, the U.S. is already involved in the Chinese liquidity problem. Some portion of excess Chinese liquidity inevitably spills into the U.S.-and more than anywhere else, because the yuan is tied to the dollar. Most famously, this was part of the feedback loop that contributed to the recent financial crisis. It has continued since, with Chinese money entering the U.S. in various ways.

But, as it was before the financial crisis, Chinese liquidity overflow into the U.S. remains only part of the loop. Though American money supply is now smaller, the U.S. economy is still much bigger, and the dollar is the world's reserve currency. Extra American liquidity, whether due to low interest rates in the middle of the last decade or quantitative easing more recently, spills over onto the rest of the globe.

When it finally becomes willing to deal with its own monetary problems, Beijing will therefore cast a nervous eye to the Federal Reserve. To a lesser extent, the Fed should do the same with regard to the People's Bank. The U.S. should:

- Continue and enhance information exchange with China on monetary policy. Countries make their own monetary choices, but transparent and timely communication helps make for better policy.

- Plan for notable economic change in the PRC in the medium term. Beijing could adopt financial reform and become much more efficient, or it might refuse and see true growth slow considerably.

- Intensify bilateral and Asian regional trade and investment liberalization, such as the Trans-Pacific Partnership, to help protect friends and allies against a possible Chinese slump.

Tightening the Taps Together?

China and the U.S. face the same long-term challenge to unwind money growth. The two challenges are connected, though the PRC's is clearly more daunting. China must act or lose monetary policy as a tool, and American policymakers should be aware of the stakes.

Forex: EUR/USD in further lows, EMU data - FXStreet.com

Forex: USD/CHF up on solid greenback, KOF - FXStreet.com

Money Saving Queen And Just Between Friends Form Partnership - News On 6

FOREX-Euro gets a lift from EU comments, but more losses seen - Reuters UK

* EU Commission comments lifts euro from lows

* Euro hits near 2-yr low vs dollar; dollar index at 20-mth high

* Focus on rising Spanish debt yields and risk of bailout (Recasts, adds quote)

By Anirban Nag

LONDON, May 30 (Reuters) - The euro bounced from near two-year lows against the dollar on Wednesday, after the European Commission called for sweeping reforms to restore investor confidence, but gains were likely to be fleeting on growing concerns about Spanish banks.

The European Commission said the euro zone should move towards a banking union and consider eurobonds and the direct recapitalisation of banks from its permanent bailout fund as it laid out year-long recommendations in a report.

The euro rose to as high as $1.24684 from a 23-month low of $1.24241 on trading platform EBS after the comments, but analysts said any bounce would only provide a fresh opportunity to sell the common currency.

"We will sell into this bounce as these proposals will take a long time and will entail changes to the treaty," said Geoffrey Yu, currency strategist at UBS.

Earlier the euro fell to its lowest since early July 2010, as real money and institutional investors stepped up sales of the currency. Their selling gathered pace as concerns grew about Spain's ailing banking sector and soaring borrowing costs, and after Italy was forced to pay dearly to sell debt.

The euro was seen highly vulnerable to further falls, with many analysts looking for a drop towards $1.20.

Concerns are growing that Spain may have to tap debt markets at a time when bond yields are near unsustainable levels. Market players fretted that it may be forced to seek an international bailout.

Adding to the euro's woes, Italian 10-year government bond yields topped 6 percent as sentiment on the indebted economy looked vulnerable to contagion from Spain's worsening problems.

"The euro is in an extremely vulnerable position and downside risks are very strong indeed ... The Spanish banking crisis has the potential to knock the stuffing out of the euro zone irrespective of the Greek election results," said Jane Foley, senior currency strategist at Rabobank.

"The issues for Spain are undoubtedly huge and most people are coming round to the idea that it will need to go outside of its borders for assistance. The longer it delays, the more the risk of a bank run."

More falls could see the euro test a reported options barrier at $1.2400. Below there it has little chart support until $1.2151, a low hit in late June 2010, and then the 2010 low of $1.1876.

The common currency also lost more than 1 percent against the safe-haven yen, taking it to a four-month low of 98.274 yen. It recovered to trade at 98.425 yen, still down 0.9 percent on the day.

DOLLAR BUOYANT

A government source told Reuters on Tuesday that Spain would likely recapitalise Bankia, which asked for 19 billion euros on Friday, by issuing new debt and possibly drawing cash from the bank restructuring fund and Treasury reserves.

The euro's weakness benefited the safe-haven dollar and yen, helping the dollar index, which measures its value against a basket of currencies, rise to a 20-month high of 82.749.

Technical analysts said a monthly close about the 100-month average in the dollar index around 81.82 may herald a shift in the longer-term trend of the dollar and reverse a multi-year drift lower.

The dollar also rose to a 15-month high against the Swiss franc at 0.9666 francs on EBS.

The higher-yielding Australian dollar fell 0.7 percent to $0.9777, slipping towards a six-month low at $0.9690, after weaker-than-expected retail sales data underscored the case for interest rate cuts. (Additional reporting by Jessica Mortimer; Editing by Andrew Roche)

Money Man Pulls Even With Black Guy In Latest Poll - The Onion (satire)

WASHINGTON—With the election less than six months away, a nationwide Gallup poll released Wednesday found that Money Man has now pulled even with Black Guy in the 2012 presidential race.

Citing Money Man's significant appeal among veterans—as well as his narrow lead in Florida, a crucial swing state that went to Black Guy in 2008—experts said Money Man is closing the gap on a race that, until quite recently, seemed to be firmly under Black Guy's control.

"I have to say, Money Man has really impressed me lately," said poll respondent Mike Hargett, who is among the 45 percent of independent voters planning to cast a ballot for Money Man in November. "I voted for Black Guy in the last election, but I’ve been fairly disappointed with the job he’s done. As much as I admire Black Guy and his historic achievement, it just seems like the time is right for someone new with fresh ideas to come in and shake things up a bit."

"Someone like Money Man," Hargett added.

Still, Money Man’s current one-point lead over Black Guy is within the Gallup poll’s margin of error, and Washington insiders have pointed to several encouraging signs for Black Guy, who maintains strong ratings on foreign policy and a double-digit lead in favorability among middle-class voters—two areas in which Money Man typically hasn’t polled very well.

Further highlighting the closeness of the race, the poll revealed there are a significant number of undecided voters still weighing the merits of a Money Man presidency vs. a Black Guy presidency.

"It's a tough choice, because both Money Man and Black Guy have strong qualities," said 47-year-old voter Albert Dorin, adding that he may not make up his mind until he sees Money Man and Black Guy next to each other on a stage, debating. "I like Money Man’s views on the economy and on money. However, you have to hand it to Black Guy for finally tracking down and killing bin Laden. And I like his wife, Black Lady, too."

"I like her more than Money Man’s wife, Blonde Lady," Dorin added.

Despite Money Man's rise in the polls, surveys have found that a majority of Republican voters would have preferred to see Food Man from New Jersey on the ballot, had he chosen to run, and that there also would have been strong support for The Woman, especially among the conservative base.

"Food Man from New Jersey or The Woman would have been more in line with my sensibilities, but there's still a good chance Money Man will pick one of the two as his running mate," Ohio voter Margaret Yaster told reporters. "Besides, for me, pretty much any Republican would be better than Black Guy. Even Pizza Black Guy."

"Not Ron Paul, though," Yaster continued. "That guy's out of his goddamn mind."

MONEY MARKETS-Speculation of ECB interest rate cuts returns - Reuters

* Markets pricing small probability of ECB rate cut in June

* Such bets likely to accumulate in coming days

* As in May, markets could set themselves up for letdown

By Marius Zaharia

LONDON, May 30 (Reuters) - Bets that the ECB will cut interest rates next week are again appearing in money markets, as Spanish and Italian debt yields are approaching levels that made the central bank introduce unprecedented easing measures last year.

The threat that Greece could eventually leave the euro and worries over Spain's banking sector have prompted investors to sell Spanish and Italian debt, bringing the two countries' borrowing costs closer to levels deemed as unsustainable.

The sheer size of their debt markets and their deep-rooted connections with other financial systems in the euro zone are reasons for investors to speculate that a policy response is in the works.

The European Central Bank is, as usual, seen as the most likely institution to take measures to cool market nerves because it can act faster than politicians. It has done it before in the past by injecting around 1 trillion euros of cheap loans into financial system in December and February.

Euro zone economic data this month has also been poor, supporting bets that the ECB may soon resume monetary easing, possibly by cutting its key refinancing rate by 25 basis points from a record low of 1 percent.

"Data ... have been softer, and then you have the Greece issue continuing to be unresolved and the Spanish issue continuing to be unresolved," said Elaine Lin, a rate strategist at Morgan Stanley, whose economists predict a rate cut.

She said the euro overnight Eonia rate forward market was only pricing an over 10 percent probability of a rate cut in June and the chances were higher by another 10-20 percentage points for the July meeting. However, she expected markets to factor in a higher probability in the next few days.

A key rate cut, if also accompanied by a cut in the 25 basis points deposit facility rate, could trigger a 5-10 bps fall in the near-term forward Eonia rates towards the 20 bps level seen now in September-October Eonia forward rates, Lin said.

The lowest point on the 2012 Eonia curve is December, at 16 basis points, which implies an 80 percent probability that the deposit rate would be slashed in half, according to BNP Paribas rate strategist Matteo Regesta.

A Reuters poll of economists showed the ECB was likely to resist pressure to cut interest rates in June, but also pointed to a growing probability that it will reduce them later this year.

Speculation about ECB monetary easing has also been fuelling a rally in Euribor futures , implying bets for lower fixings of benchmark euro zone interbank three-month Euribor rates later this year.

The December Euribor future has gained back most of its losses made since Greece's inconclusive election on May 6, which sparked fears the country may be on its way out of the bloc. The fall earlier this month also coincided with unwinding bets that the ECB would have cut rates in May.

The contract was last 3.5 ticks higher on the day at 99.46. That was one tick lower than the pre-election close on May 4, but some 15 ticks higher from the lows hit in mid-May.

The move higher in Euribor futures, which has been faster than the move lower seen in the very low Eonia forward rates, has led to tighter Euribor/Eonia spreads, which are widely used as a gauge of money market stress.

That is counter to what is happening in banking credit default swap markets - where investors can insure against banking defaults. The Markit iTraxx index of European senior financials CDS remains close to its highest level this year at around 300 bps.

BNP Paribas' Regesta warned that Euribor futures could fall again as they have done after the ECB's May meeting and this would trigger a widening of the Euribor/Eonia spreads consistent with the levels of stress felt in money markets.

"You have a decoupling between those spreads and the banks CDS now, but those spreads remain exposed to significant paying interest in coming weeks ... unless there is another policy response from the ECB at its meeting next week," Regesta said.

No comments:

Post a Comment