Time to end the live blog for the day. Here's a closing summary:

• G7 finance ministers and central bankers have discussed the eurocrisis by phone today as fears grow that Europe could trigger a new panic in the global economy. On the call, leaders discussed plans for closer fiscal union across Europe, which increasingly looks like the only way to stem the crisis.

• Spain's prime minister warned that the country is now in a situation of "extreme difficulty". Mariano Rajoy said it was imperative that Europe proves that the euro is irreversable, by agreeing a banking union and embracing eurobonds. Germany, though, remained opposed to allowing Spain's banks to be bailed out without a formal request from the Spanish government.

• A grim set of economic data showed that the eurozone economy is shrinking. Private sector output across the single currency region fell by its fastest rate in almost three years, while retail sales fell 1% and Germany factory orders also dropped. Economists predicted that the eurozone could shrink by 0.5% in the current quarter, putting more pressure on the ECB (which meets to set eurozone interest rates tomorrow).

• With the City closed for business, European stock markets had a mixed session. In quiet trading the French CAC closed 1% higher, the German DAX was broadly unchanged, and the Athens market tumbled by 5%.

We'll be back tomorrow morning. Thanks, and goodnight!

Tomorrow will be interesting - the European Central Bank will hold its monthly rate-setting meeting, Eurostat will announce the second estimate of eurozone GDP for Q1 2012, and traders will return to their desks in the City after a four-day break.

The ECB is expected to leave rates unchanged at 1%, but a shock cut can't be ruled out (especially after the poor economic data this morning).

Speaking of developing economies (see last post), it emerged earlier today that India has drawn up contingency plans for Greece to exit the euro.

"Yes, India does have a contingency plan. There are different crisis management groups within the government to deal with such a possible scenario," Kaushik Basu, the chief economic adviser to finance minister Pranab Mukherjee, told Reuters.He declined to give details of the plan, but another senior official familiar with the planning said the finance ministry and central bank were prepared to take monetary and fiscal measures if necessary to try to insulate India from the shockwaves of a euro zone collapse

One of Barack Obama's top officials has warned this afternoon that the troubles in the eurozone are the biggest threat to the global economy, and that there are already signs of a slowdown in the developing world.

Michael Froman, a senior adviser to the US President, made the comments while attending a panel discussion in Washington. They show that the American government is determined to push for a new push on economic growth at the G20 summit in Mexico in two weeks.

Here are Froman's key quotes (via Reuters):

There's an overwhelming consensus that the focus is on growth, the need for growth (and) the risks to growth around the world...The euro zone crisis is the most significant threat to growth but we see slowing growth in the developing economies.

There was some evidence of this from Vietnam earlier today, where the government warned that the Vietnamese economy might only grow by 5.2% in 2012. While most European countries* would snap your arm off for such GDP expansion, it's actually a downgrade on last month's estimate of 5.6% to 5.8% expansion.

* although not Estonia...

The word from Westminster tonight is that British officials are describing today's G7 teleconference call as a 'stocktaking session', ahead of the upcoming G20 summit.

That backs up Jeremy Cook's point about the big decisions being saved for the Mexico meeting in two week's time (see 5.04pm).

Spanish news wire AGI has a bit more detail of Mariano Rajoy's comments to the Spanish parliament:

Addressing the Spanish Senate, PM Rajoy said the EU has a duty to support financially troubled partners. "Europe must clarify what path it wishes to follow to ensure greater unity; it must clearly state that the euro is an irreversible project and that the euro is not in jeopardy; [Europe] must help nations in need.

So, as indicated earlier (3.59pm) Rajoy is making his bluntest call yet for assistance from the rest of the EU. However, Madrid's reluctance to ask for help itself (rather than simply for its banks) remains a hurdle which neither side can negotiate.

As my colleague Ian Traynor reported earlier (1.47pm), German politicians of all shades are adamant that national banks cannot simply tap the European bailout fund for help.

Someone has to blink - and World First's Jeremy Cook reckons it must be Madrid, telling us by email that:

Spain's banks are like a tinderbox at the moment but their salvation rests in the hands of politicians - a apocalyptic mix of systemic importance and staggering ineptitude. The bank guarantee scheme is a great idea until the Germans get involved and say no; as with most plans for the eurozone at the moment.Although politically destructive and obviously humiliating, it is time for Spain to ask for help from the IMF.

City analysts reckon that the G7 may be keeping its powder dry today, so that world leaders can make a big bang when the G20 meets in Mexico in two weeks time.

Jeremy Cook, chief economist of World First, said this would explain the lack of an official statement after today's teleconference. He told us:

It's not really surprising that the G7 haven't released some form of post-meeting communique; it wasn't expected and the markets have not bothered to ask for one.

The G20 meeting in Mexico in a fortnight could, and probably should, be the place for some sort of announcement as it may be able to counteract any negative news coming from the Greek elections over the weekend.

France's stock market managed a decent recovery today, despite the lack of apparent progress made by the G7. The German market also clawed back its losses, to end almost unchanged.

DAX: down 8 points at 5969, -0.15%

CAC: up 31 points at 2986, +1.07%

The Greek stock market has closed at a new 22-year low, after another day of heavy falls among banking stocks.

The main Athens index closed -5.09%. Traders said the latest selloff was partly due a prediction from Standard & Poor's yesterday that there was a 1 in 3 chance of Greece leaving the euro.

Spain's Mariano Rajoy is speaking in parliament now, and giving the clearest signal yet that Spain needs help.

Rajoy told MPs that Spain is now in a situation of "extreme difficulty", adding that Europe must now 'reinforce' the Euro project – which looks like code for closer fiscal ties, and perhaps the kind of Federal Europe which is now being considered (see today's frontpage story).

The embattled prime minister also told the Madrid parliament that Europe must declare that the euro project is "irreversable".

Rajoy also expressed strong support for a eurozone banking union, and the introduction of eurobonds – two issues which Germany will not accept until closer fiscal is agreed (as confirmed by Wolfgang Schäuble earlier today - see 11.52am)

The US Treasury has just issued its official statement following the teleconference held by G7 finance ministers earlier today.

It's not exactly a hummdinger, but it does reveal that leaders discussed the important issue of closer fiscal ties across Europe.

The G7 Ministers and Governors reviewed developments in the global economy and financial markets and the policy response under consideration, including the progress towards financial and fiscal union in Europe. They agreed to monitor developments closely ahead of the G-20 summit in Los Cabos.

Treasury secretary Timothy Geithner & Federal Reserve chairman Ben Bernanke were both on the call, we believe.

Our Wall Street correspondent Dominic Rushe isn't too impressed, commenting:

The US Treasury is clearly being very cautious and has put out a statement on the G7 meeting that takes bland to a whole new level.

Wall Street has opened for trading, with no real reaction to the news that the G7 teleconference call ended without major fanfare.

The Dow Jones is just 1 points lower at 12100, with the S&P and the Nasdaq both effectively flat. So no relief rally in New York, but no panicky selloff either.

Our Wall Street correspondent, Dominic Rushe, reports:

Yesterday the markets were down 17.11 points, or 0.14%, the fourth consecutive day of losses. Overall the Dow is so far down 479.23 points, or 3.81%, over the four-day period.

But so far it's hardly a Euro-catastrophe. Last week's awful jobs report had the biggest impact on US markets, which seem to be betting that Europe will have to reach some sort of deal. Of course if it doesn't, all bets are off.

There's a sense of anticlimax now that the G7 call has ended, without any clear progress (see 1.53pm)

Investors are growing ever more impatience at Europe's failure to make progress.

Rick Meckler, president of investment firm LibertyView Capital Management in New York, warned that that markets need to see 'concrete plans' soon. He told Reuters that finance ministers can't calm the situation by simply talking:

It has come to a point where the market needs to see some concrete plans....They took comfort in leaders getting together and talking in past times. This time they need to see something definitive to begin to resolve this crisis.

Japan's finance minister Jun Azumi has also caused some concern by telling reporters in Tokyo that the possibility of Greece leaving the eurozone was not discussed (despite the general election being just 12 days away).

What did they talk about, Spanish Banks then? RT @saraeisenFX: G7 didnt discuss Greece leaving the euro: Japan's Azumi

— Robert Passarella (@robpas) June 5, 2012

Breaking news -- the G7 teleconference call has ended.

Disappointingly, there does not appear to be a joint statement (this could change...), but Japan's finance minister Jun Azumi has been discussing the call.

According to newsflashes on the wires, Azumi is explaining that the G7 "agreed to work together to deal with the problems in Spain and Greece". He personally told the call that the current strength of the yen is damaging the Japanese economy, but added that Japan remained its confidence in Europe's response to the crisis.

No mention of 'Germany bashing', though, as one G7 member (not, I think, the UK) was predicting before the call began (see 12.08pm).

Spain's hopes that the eurozone might directly recapitalise its stricken banks without the Rajoy government actually requesting a bailout have been set back by both sides of the political divide in Germany, our Europe editor Ian Traynor flags up from Brussels.

It appears that German politicians remain sticklers for the rules that say only a government can access the bailout kitty, invariably with draconian strings attached.

Ian reports:

The parliamentary leaders of Angela Merkel's Christian Democrats and the opposition Social Democrats are both in Brussels today. They have both urged Mariano Rajoy to hurry up and ask for help while stressing that the rules can't be bent.

Volker Kauder, the CDU's parliamentary leader in Berlin, said there was no point in discussing any other kind of help for Spain.

"Discussions over a new type of aid don't seem very productive in the current situation....The help must be requested by the state concerned, as the rules prescribe. If there is now a debate about the need to recapitalise Spanish banks, the government in Madrid should promptly decide whether it wants access to the EFSF [current temporary eurozone bailout fund]."

Frank-Walter Steinmeier, former German foreign minister and current SPD parliamentary leader, was even stronger in pressing Rajoy to ask for help. "I see a risk that Spain will be too late in deciding to seek protection from the euro rescue umbrella," he said. He was sure that Rajoy would need to request a bailout.

"Spain is in a difficult situation and it's up to Europe to act. The action will be needed very soon....One should try to stabilise the banks conventionally, that is with conditions, via aid to the state."

Referring to Spanish pleas for a direct recapitalisation, supported by France and the European Commission, Steinmeier said: "I am more cautious perhaps than many of the others in this public debate."

John Maynard Keynes, who was born on this date in 1883. Photograph: Topical Press/taken from picture library

John Maynard Keynes, who was born on this date in 1883. Photograph: Topical Press/taken from picture library A quick historical note. Today is the 129th anniversary of the birth of John Maynard Keynes, and the 79th anniversary of the United States coming off the gold standard.

JM Keynes was born on this day in 1883 in Cambridge, going on to reshape economic thinking with his theories of how governments could, and should, use interventionist fiscal policies to regulate the financial cycle and prevent downturns becoming slumps. His theories remain controversial, but advocates argue that Keynesian economics remains our best hope of avoiding another Great Depression (eg, yesterday's interview with Paul Krugman).

Keynes made his reputation during the financial crisis of the 1920s and 1930s, when politicians and central bankers wrestled with the biggest financial panic of the last century. That crisis led to the various leading economies dropping off the Gold Standard as the pillers of the financial system crumbled. America took the plunge on 1933, when Franklin D Roosevelt signed the legislation meant America would no longer peg the dollar to a fixed gold price (although it took until the 1970s for Nixon to finally break the link).

Incidentally, today could also be the anniversary of the birth of ground-breaking political economist Adam Smith (there's some ambiguity about exactly which day he was born in 1723)

Our understanding is that UK chancellor George Osborne is taking part in the G7 call to discuss the eurocrisis.

There's no official word about how the call is going, but an Italian government officials has told the FT that the call is basically a follow-up to the discussion which took place two weeks ago when the G8 met in America.

That suggests that the issues of eurozone bank recapitalisation and growth strategies could dominate the call...

French foreign minister Laurent Fabius has weighed in over the Spanish banking crisis today, telling a conference in Paris that banking union could help address the crisis.

Fabius argued that a solution must be found that does not add to Spain's own debts, at a time when its bond yields are already dangerously high.

Fabius said:

We have to find mechanisms, methods to bring the necessary funds to allow the system to continue to function properly without adding to Spain's budget deficit, otherwise we won't get anywhere....If, to save the bank, you have to increase the deficit and this increase leads to higher interest rates, then it's the snake eating its tail.

He added that France would "favour" a solution based around a banking union.

Of course, Fabius isn't completely impartial here. French banks hold a lot of Spanish debt, and would also benefit from closer banking ties across the eurozone.

So, where are we with Spain? After weeks of deadlock, it does feel as if its banking crisis is close to some kind of resolution.

The key sticking point remains Spain's extreme resistance to taking any form of official bailout. As reported at 12.08pm, that is irking some members of the G7, with Reuters reporting this lunchtime that Madrid's "fatal hubris" is causing some alarm.

The Spanish government does appear to be giving some ground. Treasury minister Cristobal Montoro admitted this morning (see 9.17am) that European institutions need to "open up" and help the country recapitalise its banks.

The hitch, though, is that Europe's bailout funds cannot, as currently defined, pump money into a national banking system directly.

Looking briefly at the currency and commodity markets, the euro has lost more than half a cent against the US dollar this morning. From $1.2490 overnight, the euro has now dropped to $1.242.

The pound is also down against the US dollar, trading around $1.5343.

The strengthening dollar has also pushed down the oil price, with a barrel of Brent crude down 81 cents at $98.04. And the gold price is flat, at $1,618 per ounce.

A source at a G7 country has told Reuters that today's G7 conference call is likely to turn into a "Germany bashing session".

That suggests the US, the UK, France, Italy, Japan and Canada may be taking a united position that Germany needs to change its approach to the crisis.

Reuters' G7 source also says that Germany is "pushing Spain' to take help from the European bailout fund to recapitalise its banks, but that Madrid is currently resisting.

From the terminal:

"They don't want to. They are too proud. It's fatal hubris," the source said of the government in Madrid.

That fits with reports that Spain has been privately pushing for help for its banks without the Spanish state having to take an aid deal. Under the current rules, of course, the European Stability Mechanism cannot directly recapitalise European banks (although many players, including the IMF, think it should able to).

Officially, Germany has been arguing that Spain has been 'everything right'.

German finance minister Wolfgang Schäuble has given an interview to Handelsblatt, in which he reiterates Berlin's position that "a real fiscal union" must be created before more contentious issues such as eurobonds can be considered.

Schäuble told the business daily that closer fiscal ties remain the first step, and even that is a 'medium-term' objective. Banking union could come later, but Schäuble didn't indicate it could happen quickly, saying:

We should take one step after another

There's some more detail here and here.

Schäuble should be on the G7 conference call, starting soon...

An interesting development in the Italian banking sector today – Alessandro Profumo, the former chief executive of UniCredit, has today been indicted in a tax fraud case, according to reports from Milan.

Profumo is one of 20 bankers charged with alleged tax fraud. According to Bloomberg, several other former Unicredit execs are also facing trial, along with some former staff from Barclays. Details here.

The European Union has said that the G7 conference call (due to start in 25mins) will allow the EU to update its partners on the region's response to the ongoing crisis.

At the regular midday briefing, an EU spokesman also explained that the G7 call is part of a "regular exchanges of views", so we shouldn't panic just because finance ministers are talking.

It's not clear, though, which EU officials will be on the call:

EU says cannot yet confirm if EU's Rehn will take part in the G7 call

— Fabrizio Goria (@FGoria) June 5, 2012

City analysts and traders hope that the G7 can make some headway in their conference call at noon BST, but they aren't terribly confident.

Michael Derks, chief strategist of currency trading site FxPro, commented:

Frankly, given the incredibly fragile sentiment evident over recent weeks, the G-7 needs to come up with something fairly convincing to soothe the nerves of traders and investors alike.

A man walks past a board showing graphs of Japan's stock price indexes outside a brokerage in Tokyo, earlier today. Photograph: Toru Hanai/Reuters

A man walks past a board showing graphs of Japan's stock price indexes outside a brokerage in Tokyo, earlier today. Photograph: Toru Hanai/Reuters News of the talks did help push shares higher in Japan overnight, where the Nikkei finished 1% higher. There's less optimism in Europe, though, with German shares lower, and Wall Street expected to open slightly lower (but that could change, depending on how the G7 call goes)

Another piece of poor economic news – German industrial orders fell by 1.9% in April. That is the biggest drop since last November, and worse than expected (economists had predicted -1.1%)

Yet another sign that the eurozone economy has deteriorated in recent months - although the German economy ministry did point out that March had seen surprisingly strong growth, so a fallback in April shouldn't be a shock.

Reuters is reporting that G7 finance minister will hold their conference call to discuss the eurozone crisis at 11am GMT, so in an hour and half's time.

More euro economic gloom -- retail sales across the single currency region fell by 1.0% in April, compared with March. That's the biggest monthly fall since last December.

On a year-on-year basis, retail sales were 2.5% lower than a year ago.

Howard Archer of IHS Global Insight said it was "a dismal day for the Eurozone on the economic front" (with the service sector shrinking at its fastest rate in almost three years).

After an early rally, European stock markets have dropped back, with Germany's DAX in the red again:

DAX: down 54 points at 5923, - 0.9%

CAC: up 7 points at 2962, + 0.26%

IBEX: up 20 points at 6260, + 0.29%

That follows the news that Eurozone private sector shrank again last month (see 9.36am)

Traders work at the stock exchange in Frankfurt yesterday. Photograph: Daniel Roland/AFP/Getty Images

Traders work at the stock exchange in Frankfurt yesterday. Photograph: Daniel Roland/AFP/Getty Images German shares also fall yesterday, on concerns that its exporters will suffer from a global economic slowdown, or worse, if the eurozone crisis is not resolved.

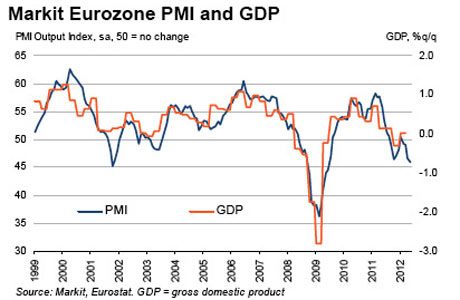

Europe's service sector has suffered its worst monthly decline in almost three years, in the latest evidence that the region's economy is shrinking.

Markit reported its latest PMI data this morning, and the picture across Europe was pretty bleak. Germany's service sector grew at its weakest amount for six months in May, while most other countries' sectors shrank:

Germany: 51.8 (where >50= growth, and <50=contraction)

Spain: 41.8

Italian: 42.8

France: 45.1

When combined with last Friday's manufacturing data (which was also grim), the data shows that the Eurozone's private sector shrank at its fastest pace since June 2009. At 46.0, May's 'composite PMI' was the fourth month in a row to show a contraction. Even Germany's output fell, although at a slower rate than the rest of the eurozone.

Latest economic data shows Europe's economy is shrinking.

Latest economic data shows Europe's economy is shrinking. Chris Williamson, Markit's chief economist, said the data suggests eurozone GDP will fall by as much as 0.5% this quarter (having stagnated in Q1).

There is some convergence among member countries, but unfortunately only in the sense that all of the largest are now experiencing downturns. While Germany is contracting only marginally, alarmingly steep downturns are evident in Spain, Italy and now also France.

Italy seems to be faring the worst, with its PMI consistent with GDP falling by more than 1% in the second quarter.

Spain's Treasury minister has caused some disquiet this morning by stating that the country is effectively shut out of the bond markets -- just two day before it holds a debt sale.

Cristobal Montoro also appeared to signal that Spain needs international help, but not a full bailout, in an interview with Spanish broadcaster Onda Cero.

Montoro told the radio station that:

The risk premium says Spain doesn't have the market door open...The risk premium says that as a state we have a problem in accessing markets, when we need to refinance our debt.

Spain's 'risk premium', measured by the difference between the yield on its 10-year bonds and the German equivalent hit record levels last week. As I type, the spread between the two bond yields is 515 basis points - a massive difference in borrowing costs.

Spain is due to auction €2bn of medium-term debt on Thursday.

Montoro expressed strong support for Europe to create a closer "banking union", saying a decision should be taken at the next EU summit at the end of June. He also argued that "European institutions" should provide funding to help recapitalise its banks, saying Spain needs to show how it will strengthen its banking sector.

That's why it's so important that the European institutions open up and help us achieve, help facilitate, that figure because we're not talking about astronomical figures.

Bloomberg reckons this is the first time a Spanish minister has called for outside funds. Prime minister Mariano Rajoy has long argued that the European Stability Mechanism should be able to recapitalise European banks directly (rather than via the state), without going as far as to state that Spain needs their help.

Montoro also said it was 'technically impossible' to bailout Spain itself – an acknowledgement that Europe's firewall isn't strong enough.

Britain saw its credit rating cut by one notch last night, by ratings agency Egan Jones.

Egan Jones slashed the UK's rating by one notch to AA-minus, from AA, and left a negative outlook on the rating. It warned that Britain may fail to trim its deficit as quickly has planned, saying in a statement that:

The over-riding concern is whether the country will be able to continue to cut its deficit in the face of weaker economic conditions and a possible deterioration in the country's financial sector

Not a very nice way to mark the Queen's Diamond Jubilee...

Egan Jones isn't one of the Big Three rating agencies, and at present it rates many countries as more of a credit risk than Moody's, S&P or Fitch.

Our Europe editor, Ian Traynor, argues in today's Guardian that a "United States of Europe" may be the only way to save the eurozone. Here's a flavour:

The USE – United States of Europe – is back. For the eurozone, at least. Such "political union", surrendering fundamental powers to Brussels, Luxembourg and Strasbourg, has always been several steps too far for the French to consider.

But Berlin is signalling that if it is to carry the can for what it sees as the failures of others there will need to be incremental but major integrationist moves towards a banking, fiscal, and ultimately political union in the eurozone.

It is a divisive and contested notion which Merkel did not always favour. In the heat of the crisis, however, she now appears to see no alternative.

The next three weeks will bring frantic activity to this end as a quartet of senior EU fixers race from capital to capital sounding out the scope of the possible.

As Rainman2 points out in the reader comments, three of Portugal's banks are being recapitalised to the tune of €6.6bn.

The move will mean Banco Commercial Portugues, Banco BPI and Caixa Geral de Depósitos can all hit Europe's tougher capital reserve requirements. The money is coming from Portugal's €78bn bailout (agreed last year, which included €12bn for its financial sector).

Crucially, Portugal is still meeting the terms of its rescue package, despite fears that a second bailout might be needed. Its Troika of lenders announced last night that the Portuguese financial reform programme "remains on track amidst continued challenges." That decision means Lisbon will receive its next tranches of aid, totalling €4.1bn.

The financial markets, though, are still pricing Portugal as a serious risk. It's 10-year bonds are trading at a yield of around 11.5% today, deep into the 'danger zone'.

Canada's finance minister Jim Flaherty. Photograph: Chris Wattie/Reuters

Canada's finance minister Jim Flaherty. Photograph: Chris Wattie/Reuters The news that G7 finance chiefs are to hold a teleconference call today is a clear signal from the world's largest economies that the Eurozone must take rapid steps to stem the crisis.

The call was first revealed by Canadian finance minister Jim Flaherty last night. He told reporters that ministers and central bankers from Canada, the US, Britain, Japan, Germany, France and Italy would hold a special conference call to discuss the eurozone crisis, explaining that:

The real concern right now is Europe of course – the weakness in some of the banks in Europe, the fact they're undercapitalised, the fact the other European countries in the eurozone have not taken sufficient action yet to address those issues of undercapitalisation of banks and building an adequate firewall.

This mesage was reiterated by the US government, with White House press secretary Jay Carney warning that "more steps need to be taken" to address the crisis and reassure the financial markets.

And overnight, Japan's finance minister, Jun Azumi, also confirmed that concerns over the eurozone crisis are now dangerously high, warning:

We have reached a point where we need to have a common understanding about the problems we are facing.

G7 conference calls are usually confidential, so Flaherty's decision to go public may indicate that world leaders are keen to apply the maximum pressure to the eurozone. We don't yet know when the call is taking place.....

Here's a quick agenda of some of the main events and economic data coming up:

• G7 finance ministers hold conference call: timing currently unknown

• Eurozone purchasing manager index on services for May: 9am BST

• Eurozone retail sales for April: 10am BST / 11am CEST

• German factory orders for April: 11am BST/ noon CEST

• Bank of Canada's interest rate decision: 2pm BST/ 9am EDT

Good morning, and welcome back to our rolling coverage of the eurozone financial crisis.

After a day off yesterday to toast her Majesty and put up more bunting, we're back to track the latest action across Europe. The key development this morning is that G7 finance ministers are due to hold emergency talks on the euro zone debt crisis later today. More on this shortly.

Across Europe, pressure is growing on Germany to accept a 'banking union' across Europe. As my colleagues Ian Traynor and Giles Tremlett report:

Europe's leaders appear to be edging towards an ambitious and controversial new blueprint for a federalised eurozone after Paris and Brussels threw their weight behind Spain's pleas for an EU rescue of its beleaguered banks.

At the start of three weeks likely to be crucial to the survival of the euro, the new French government and the European commission voiced strong backing for a new eurozone "banking union" to save the single currency.

The plan could see vast national debt and banking liabilities pooled – and then backed by the financial strength of Germany – in return for eurozone governments surrendering sovereignty over their budgets and fiscal policies to a central eurozone authority.

A "gang of four" – the European council president, the commission chief, the president of the European Central Bank and the head of the eurogroup of 17 finance ministers – has been charged with drafting the proposals for a deeper eurozone fiscal union, to be presented to an EU summit at the end of the month.

Things may be quieter than normal, with the UK enjoying another bank holiday today. But other European markets will be trading as usual, after a mixed day yesterday, so there should be plenty to report. There's also some interesting economic data due, covering the world's service sectors, eurozone retail sale, and German factory orders.

FOREX-Euro hits 1-week high as bears trim bets ahead of G7 call - Reuters UK

* Euro hits 1-week high vs USD, above tenkan line

* Euro rebound may lose steam if no concrete steps from G7

* Some speculate ECB might act on Wed

* Aussie gains after 25 bp cut, market expects more cuts

* Short-term dlr/yen call options in favour on intervention fears

TOKYO, June 5 (Reuters) - The euro extended gains to a one-week high on Tuesday as some sellers pared back their huge bets against the currency ahead of a conference call by the Group of Seven financial policy makers on the European debt crisis.

Although market players remain sceptical of a major breakthrough given a lack of consensus within Europe on how to save Spanish banks and on other matters, there was caution in case the meeting leads to some kind of policy agreement, given record short positions on the euro.

"It will take a long time to resolve the debt crisis. I don't expect European policy makers to come to an agreement soon. I am ready to sell the euro around $1.2550," said a trader at a Japanese bank.

The euro rose to as high as $1.25429, its highest in a week, extending its rebound from a two-year low of $1.2288 reached on Friday. It last stood at $1.2520, up 0.2 percent from late U.S. levels.

On the daily Ichimoku chart, the euro rose substantially above the tenkan line for the first time in about a month and if it closes above that level, at $1.24565 on Tuesday, it could herald further recovery in the battered currency.

Immediate resistance for the euro lies at $1.2545, the 76.4 percent Fibonacci retracement of its decline last week and above that there is resistance at $1.2570, the 23.6 percent retracement of its longer term decline from a February high of $1.34869.

Against the yen, the single currency rose 0.3 percent to 98.22 yen, moving off Friday's 11-year low of 95.59 yen. It hit a fresh one-month high against the British pound at 81.405 pence.

News that finance chiefs from the Group of Seven leading industrialised powers will hold emergency talks on the euro zone prompted some market players to speculate that the European Central Bank could yield to additional pressure.

"They may put pressure on the ECB to do something," said Eiji Kinouchi, chief technical analyst at Daiwa Securities.

Some market players said ECB President Mario Draghi may embark on pre-emptive moves and surprise markets, as he did last year just after he took over the helm at the bank. They added that the ECB could implement a rate cut or a massive injection of funds.

RBA CUTS

Financial markets are anxious about the risks from a Spanish banking crisis and fret a Greek election on June 17 could lead Athens to leave the single currency and precipitate yet more economic turbulence.

France and the European Commission signaled their support on Monday for an ambitious plan to directly use the euro zone's permanent bailout fund to rescue stricken banks.

But Germany, the euro zone's biggest economy and the biggest contributor to the European Stability Mechanism, has so far opposed any use of bailout funds without a country having to submit to a politically humiliating austerity programme imposed by international lenders.

In a sign of increasing concern about the impact of the euro zone debt crisis, the Reserve Bank of Australia cut interest rates by 25 basis points but the cut was less than some had expected, sending the Australian dollar higher .

Local money markets had been pricing in a rate cut of at least 25 basis points, with some players looking to a deeper 50 basis point cut.

The Australian dollar rose close to 0.7 percent to $0.9784 , extending its recovery from an eight-month trough of $0.9581 hit on Friday.

Still, some market players see the Aussie trapped in a downtrend as they expect the Australian central bank to cut rates further in coming months.

The Japanese yen moved little against the U.S. dollar at 78.33 yen, off Friday's 3 1/2-month low of 77.652 yen, helped by wariness about Japanese yen-selling intervention as Japanese Finance Minister Jun Azumi has stepped up his rhetoric against the yen's rise.

Some market players are buying short-term dollar/yen calls to bet on, or hedge against intervention, pushing the one-week risk reversal spread to its highest level in favour of dollar calls in six months. (Additional reporting by Antoni Slodkowski; Editing by Edwina Gibbs)

FOREX-Euro briefly extends losses vs dollar, dollar gains vs yen - Reuters

Thomson Reuters is the world's largest international multimedia news agency, providing investing news, world news, business news, technology news, headline news, small business news, news alerts, personal finance, stock market, and mutual funds information available on Reuters.com, video, mobile, and interactive television platforms. Thomson Reuters journalists are subject to an Editorial Handbook which requires fair presentation and disclosure of relevant interests.

NYSE and AMEX quotes delayed by at least 20 minutes. Nasdaq delayed by at least 15 minutes. For a complete list of exchanges and delays, please click here.

FOREX-Euro falls on Spain warning, G7 disappointment - Reuters

Thomson Reuters is the world's largest international multimedia news agency, providing investing news, world news, business news, technology news, headline news, small business news, news alerts, personal finance, stock market, and mutual funds information available on Reuters.com, video, mobile, and interactive television platforms. Thomson Reuters journalists are subject to an Editorial Handbook which requires fair presentation and disclosure of relevant interests.

NYSE and AMEX quotes delayed by at least 20 minutes. Nasdaq delayed by at least 15 minutes. For a complete list of exchanges and delays, please click here.

Money funds rates ultra low but "no place to go" - Reuters UK

* Money fund assets level off as retail investors sit tight

* Advisers see few safe alternatives for cash

By Ross Kerber

June 5 (Reuters) - The miniscule interest rates being paid by money market mutual funds are making many investors restless, but wealth advisers are urging most to stay the course.

Already historically low U.S. short-term interest rates have dipped even lower in recent weeks as investors fleeing financial turmoil in Europe have sought safe havens.

But investors have little to fear that rates could turn negative on money market funds, and alternatives like bank savings or checking accounts are no more appealing, advisers said.

"Everything that is stable is crummy," said Douglas Conoway, managing principal of Wealth Management Group LLC in Rochester, New York. "There's no place to go."

Conoway's firm invests about 5 percent of its $40 million in client assets in money funds, the same level as a year ago.

The stability of money funds does not mean investors are happy with their rates. John T. Boland, president of Maple Capital Management Inc in Montpelier, Vermont, said clients often call to complain about low rates, which he said "have given a whole new meaning to the phrase 'cash drag.'"

But there are not a lot of alternative investments he can suggest -- "which is why we are holding the cash in the first place!!" Boland wrote in an email.

Low interest rates have already forced fund sponsors to waive billions of dollars in fees to prevent yields from going negative. Fund companies have the resources to keep waiving fees and maintain yields above zero, said Peter Crane, publisher of Cranedata.com, a website that tracks the industry.

"If they haven't gone negative by now, guess what, they're not going negative," he said.

By some measures, the pressures on fund companies are easing despite the safe-haven flood into short-term U.S. government securities. While rates on Treasury bills declined, rates on other investments the funds buy such as repurchase agreements have ticked up.

Big fund sponsors like Fidelity, Federated Investors Inc and JPMorgan Chase & Co on average waive 45 percent of fund fees, down from 50 percent several months ago, Crane said.

The desire for safety should be paramount, said Philip Blancato, chief executive and president of Ladenburg Thalmann Asset Management in New York. "While there is little yield available in the market today, we continue to believe safety of assets is more important than yield," he said.

A few advisers have tried to come up with alternatives to money funds. In Westport, Connecticut, Gerard Gruber, chief investment officer of Hayden Wealth Management, said his firm might suggest a combination of municipal bonds, fixed annuities or dividend-paying stocks and funds. Only the safest money funds pass its screens, such as those that invest in government-backed instruments.

"Our clients are willing to accept a lower money market rate that invests conservatively than be with one that takes more risk and has exposure to possible losses," he said.

In Michigan, financial planner Theodore Feight said he has started replacing money fund holdings with dividend-paying stocks like those of Intel Corp and Altria Group . He also has bought high-yield corporate bond exchange-traded funds.

"Money market rates are just not cutting it anymore," he said.

Hoping to capture flows, some firms have pitched new products as money fund alternatives. On a web page about a new fund, for instance, Pacific Investment Management Co, operator of the world's biggest bond fund, writes: "PIMCO Short Asset Investment Fund offers higher income potential than traditional cash investments. ... Unlike money markets, however, the net asset value (NAV) of the fund may fluctuate."

Many of the new funds fall into the category of "ultra short obligation bond funds" tracked by Thomson Reuters' Lipper unit. Flows to these funds totaled $2.2 billion through the end of May, on pace to surpass the $3.4 billion they took in for all of 2011.

Still, that is just a drop in the bucket compared with money fund assets overall. The funds held $2.55 trillion at May 29, down from $2.65 trillion at the start of the year, according to iMoney.net. (Editing by Aaron Pressman and Leslie Adler)

Forex Flash: Today's strategy for USD/JPY – Commerzbank, Danske Bank and UBS - FXStreet.com

Smart money to follow Smartpay's leader? - Stuff

OPINION: From time to time you hear of companies complaining they cannot raise capital in New Zealand.

Kiwi investors are too conservative, too dim, too poor, too insular, too blinkered, too demanding, too risk averse and too blind to opportunity, they say, before flouncing across the Ditch to try their luck in Australia.

They may be right. On the other hand, they may just need to look in the mirror to find the cause of their troubles.

To date, Chalkie has placed Smartpay in the latter category. The eftpos systems company is involved in some clever technology most of us use every day, but since arriving on the NZX through the back door in May 2006 its performance has been, to put it politely, mercurial.

Indeed, in the last couple of years it has been more quicksand than quicksilver as the business thrashed itself ever more deeply into a quagmire of debt.

This time last year managing director Ian Bailey was trumpeting a "remarkable turnaround" as earnings before interest, tax, depreciation and amortisation hit a record $7.2 million, a 252 per cent improvement on the previous year.

Revenue, meanwhile, was apparently a respectable $47m.

The shares, then trading at about 21c, steadied briefly before resuming their downward slide the following month. Already a minnow, Smartpay was turning into a penny dreadful.

A big part of the problem involved its business model. Smartpay provides eftpos payments systems – the hardware, the software, the connection and ongoing service – for retailers who pay fees over the term of a contract of, say, three years.

But instead of doing the deal and waiting for the cash to come in, Smartpay typically sold 80 per cent of the future cashflows to third-party financiers. This allowed it to book most of the contract value as immediate revenue.

Except it was not really revenue, it was debt – and costly debt at that.

Adding to the burden was its $6m acquisition in 2009 of the payments unit of ProvencoCadmus, a business well-known to Bailey who had co-founded the Cadmus part in the 1990s.

But back to the debt.

In the year to March 2011, when revenue was $47m, the cash-flow statement said actual receipts from customers were $33.6m.

Payments to suppliers and employees, meanwhile, were $42m, and operating cash was negative $11.8m.

The gap was bridged with borrowing of $13m.

Same thing happened the previous year.

To be fair, there was logic behind the idea, which was to ensure growth was not limited by cashflow. Signing up customers entailed up-front costs, such as buying the eftpos swipecard hardware from a contract manufacturer in China, and those costs had to be financed somehow.

Unfortunately, Smartpay's solution was to borrow from a range of second-tier lenders such as FE Securities at rates as high as 18 per cent, which did not do much good for its profitability.

It also meant if the rate of signing new sales contracts slowed down, revenue would fall off a cliff.

This is exactly what happened.

Smartpay had been benefiting from rules obliging New Zealand retailers to upgrade their terminals, but by June last year the job was done and sign-ups plummeted.

Hence, the latest full year result reported last week revealed revenue down from $47m to $29m.

Indeed the result was chocker with ugly numbers.

The bottom line was a $12.7m loss and liquidity was critically low – those borrowings had driven current liabilities to $26m, well in excess of current assets of $17.6m.

Normally, we might associate these figures with the beginnings of a death spiral, but Chalkie has been intrigued to see a very different scenario emerging under the leadership of Bradley Gerdis, Smartpay CEO since December.

South African-born Gerdis, based in Sydney, has a useful track record for the job, having been a founding executive in 2004 with ASX-listed Customers Ltd, which built a network of independent cash machines in Australia.

Since leaving Customers in 2008 he has been busying himself with a few jobs at his own firm Active Capital Partners, but obviously saw an opportunity to make a difference at Smartpay.

We got a picture of the difference last week when Smartpay announced a major restructuring along with its dreadful result.

The main change involved a $13m influx of equity capital and a new $25m bank debt facility with ASB – $20m of it to revamp the balance sheet, and $5m headroom for capital expenditure.

The money allows Smartpay to buy back its contract cashflows from the second-tier financiers at a much cheaper rate, thus ensuring revenue stability in years ahead.

Gerdis describes it as "the flicking of a switch".

At balance date Smartpay had borrowings of $29.4m, most of it high cost and two-thirds of it due within a year.

The refinancing deals with that immediately and sets up the business to get $17.5m of recurring revenue a year from now on, producing earnings before interest, tax, depreciation and amortisation of about $7.5m.

At that level profitability looks within reach as interest costs on $20m will likely be below $1.5m.

"Because the previous management never really had access to the right type of capital, both debt and equity, it's been funded by very high-cost mezzanine debt and it's bled the business of the cashflow that should rightly have belonged to shareholders," Gerdis told Chalkie.

"The immediate release of equity value by making this thing cash-flow positive and self-sustaining is just tremendous. That's why we were able to raise the money at a significant premium to the market because investors understood that."

It is a fair comment. The new equity was raised at 11.5c a share. Before the announcement the shares were trading at 8-9c.

So why was Smartpay able to raise a decent chunk of money at a premium now, when it struggled to do so before?

Chalkie recalls considerable bleating from Smartpay about lack of interest from Kiwi investors and its desire to shift to Australia.

The main reason, Chalkie suspects, is that investors were not comfortable with the previous plan or the previous leadership.

For example, in 2011, the year Bailey described Smartpay as a "changed company", it still appeared to be persisting with the debt-funded model.

The annual report said: "Providing we continue to to expand the rental base, and ensure funding is in place to support the growth of the rental book, then the company will rapidly reach the point whereby the ongoing monthly cashflows will exceed all costs and overheads, leaving a residual cash component available to repay corporate debt."

This sounds like more of the same, and although there was acknowledgement of high-interest costs as the company expected to "work directly with banks as opposed to mezzanine funders as we have now", Chalkie reckons it was about as encouraging to investors as a half-time team-talk from Eeyore.

The idea now is to pick up business in Australia, where the eftpos trade has hitherto been dominated by the big banks.

Smartpay's announcement in February of a deal to provide 4000 terminals to customers of Bendigo & Adelaide Bank indicated the way forward.

Gerdis, gung ho, describes the Australian business opportunity as "real, sizeable and immediate".

"This is expected to include strong organic growth which will in all likelihood be accelerated through strategic acquisitions," he says.

He's talking a good game, clearly, but Gerdis has his money where his mouth is, having invested $1m at 10c a share in December. He also has some hefty options to subscribe for shares in future at prices starting at 15c.

Adding to the picture of a company on the move is the awarding of options on similar terms to new Australian chairman Ivan Hammerschlag, executive chairman of Athlete's Foot owner RCG.

It will be interesting to see whether the incentives produce a higher share price for investors. If it does – and after previous underperformance, let us hope so – it will be quite a turnaround story, although not a particularly New Zealand one.

- Chalkie is written by Fairfax Business Bureau deputy editor Tim Hunter.

- © Fairfax NZ News

Islamic Finance set to mobilize trade and investment flows between Asia and the Middle East - AME Info

The two day WIBC Asia event, held under the official support of the Monetary Authority of Singapore, kicked off today with an inaugural address by H.E. Ravi Menon, Governor of the Monetary Authority of Singapore.

The inaugural address was immediately followed by an opening keynote session which featured H.E. Dr. Ahmad Mohamed Ali Al-Madani, President of the Islamic Development Bank and Edy Setiadi, Executive Director of the Directorate of Islamic Banking, Bank Indonesia. The session addressed the challenges and opportunities inherent in the increasingly global geographic footprint of Islamic finance and also discussed the national and international initiatives that will ensure consistency and foster greater interconnectedness across key jurisdictions for Islamic finance.

A key highlight of WIBC Asia 2012 was the high profile Power Debate session led by internationally respected CEOs and industry leaders. Moderated by Haslinda Amin of Bloomberg Television, the session analyzed the expanding role of Islamic finance as a conduit for trade and capital flows between Asia and the Middle East and also discussed how Islamic financial institutions can better develop the capacity to structure large-scale multi-currency and cross border transactions. The Power Debate session featured Toby O'Connor, Chief Executive Officer, The Islamic Bank of Asia; Hussain AlQemzi; Chief Executive Officer, Noor Islamic Bank and Group Chief Executive Officer, Noor Investment Group; Muzaffar Hisham, Chief Executive Officer, Maybank Islamic Berhad; Dato' Jamelah Jamaluddin, Chief Executive Officer, Kuwait Finance House (Malaysia) Berhad (KFH Malaysia); Syed Abdull Aziz Jailani Bin Syed Kechik, Chief Executive Officer, OCBC Al-Amin Bank Berhad; Shamsun Anwar Hussain, Director - Consumer Banking, CIMB Islamic Bank Berhad; and Wasim Saifi, Global Head, Standard Chartered Saadiq, Consumer Banking.

Speaking to the media present at the event, David McLean, Chief Executive of the World Islamic Banking Conference: Asia Summit noted that "Asia is becoming an increasingly attractive destination for investments that are Shari'ah compliant. To reap the full benefit of the region's rapid expansion and robust development, there is a need to press on towards achieving global connectivity and deepening economic cooperation with various key centres for Islamic finance. In order to better facilitate cross-border relationships, more intensive international co-ordination of regulatory approaches, supervisory oversight and industry practices is needed."

He also said that "as interest in Islamic finance expands across Asia, an increasing number of Middle Eastern investors are looking at opportunities to deploy their capital in the region and Islamic finance is perfectly positioned to act as a catalyst to further bridge capital flows between Asia and the Middle East."

"An ongoing dialogue between key regulators, industry practitioners and market participants representing the two key centres for Islamic finance, i.e the Middle East and Asia, is vital to achieve greater international harmonization in the architecture for Islamic finance", he added.

A similar view was expressed by Hussain AlQemzi, Chief Executive Officer, Noor Islamic Bank and Group Chief Executive Officer, Noor Investment Group, who said that "in order to ensure an orderly evolution of Islamic finance from a niche segment into the mainstream international financial markets, it is vital to further enhance the industry's capabilities for cross-border activities, which in turn will encourage innovative product development, robust and standardised regulatory frameworks and the long term stability of the industry. What the industry lacks at the moment is the breadth and depth that investors enjoy in the conventional market. An inter-linkage between the key Islamic financial centres will facilitate investor access to a wider range of Shari'a-compliant products beyond those available in their domestic market."

He also said that "the annual World Islamic Banking Conference: Asia Summit is becoming an increasingly important platform that facilitates dialogues between the two key centres for Islamic finance - Asia and the Middle East. The theme for this year, "Islamic Finance in Asia: Strengthening International Connectivity and Capturing Cross-Border Opportunities", highlights the tremendous potential for significant cross-border transactions which the Islamic finance industry must tap into. As a key industry player we are keen on exploring these unique opportunities."

Commenting on their participation at the event, Toby O'Connor, Chief Executive Officer of the Islamic Bank of Asia said that "the theme for the 3rd Annual World Islamic Banking Conference: Asia Summit (WIBC Asia 2012), "Islamic Finance in Asia: Strengthening International Connectivity and Capturing Cross-Border Opportunities", highlights a significant opportunity that IB Asia is focused on. We hope that the high-level discussions at this important forum in Singapore will foster new business relationships between key growth markets for Islamic finance. We are once again delighted to renew our partnership as a Platinum Strategic Partner of WIBC Asia."

WIBC Asia 2012 continues on the 6th of June and will features an exclusive keynote address by Jaseem Ahmed, Secretary-General of the Islamic Financial Services Board (IFSB), and a special address by Daud Vicary Abdullah, President and Chief Executive Officer of INCEIF- The Global University of Islamic Finance.

Finance: Budget affects tax deductions - Wairarapa Times-Age

Industry heads and other experts have been downplaying the impact to changes in this year's Budget that will affect owners of holiday homes, boats and private planes.

While those who own private planes may perhaps not be overly concerned with tax breaks, a lot of people who have baches they rent out a couple of nights a week are set to lose the ability to claim tax deductions.

This is a case where the less often you rent a holiday home out, the more you will be affected.

Previously, holiday home owners have been able to claim tax deductions of up to 90 per cent of the general losses they incurred in the running of those homes.

That's things like loan interest, maintenance costs, and so on.

Now, how much they can claim will depend on how often the property is rented.

It will be worked out as a formula: The number of rented nights divided by the total number of nights the property is used gives the proportion that can be claimed as a tax deduction.

That means if you own a holiday home, stay there yourself 30 days a year and rent it out for 30 nights, you will only be able to claim a 50 per cent deduction, not the 90 per cent you could have claimed previously.

Similarly you won't be able to say you run a loss-making business renting your boat out a couple of weekends a year if, in fact, most of the time your boat is used for your own fishing trips.

Real estate industry experts are saying the Budget changes won't affect coastal property prices because people think of the tax breaks as a benefit, not the reason for buying a property.

Reinz chief executive Helen O'Sullivan says it's not something that affects property owners enough to really make a difference.

She points out that those who run their holiday homes as true investment properties will probably not be affected because their properties will be rented enough that the tax deductions will still apply.

The only concern will be that they may need to structure their own use to avoid the busy periods when properties will be easier to rent.

While it may indeed be the case that true investors won't be affected and everyone else just sees tax deductions as a benefit, for those who arestill deliberating on the decision of whether to buy a bach, this may be the move that changes their minds against it.

Coastal property prices are still high, international travel is as cheap as ever, and the luxury of regular weekends away is out of touch of a lot of people's busy lifestyles.

If you own an investment property, a boat that you sometimes rent out, or even private plane, talk to your accountant about how the changes might affect you.

No comments:

Post a Comment