Dubai, United Arab Emirates, 5 June, 2012 - FOREX.com, the retail division of GAIN Capital (NYSE: GCAP), a global provider of online trading services, was awarded "Best Arabic FX Platform 2012" at the recent Saudi Money Expo held in Jeddah.

FOREX.com was given the prestigious accolade based on voting by investors and industry experts ranking the top FX brokers and educators in the region.

"We are delighted to receive this award, which recognizes our commitment to tailor and improve our services for our customers in the Middle East," said GAIN's Chief Product Officer Muhammad Rasoul. Mr. Rasoul added, "Trading volume from the region grew over 150% last year and, in anticipation of continued growth in the region, we recently launched an enhanced Arabic version of our FOREXTrader PRO platform, featuring Arabic language news and research, along with fully localized trading tools."

FOREX.com offers trading in more than 70 markets, including currencies, gold & silver, oil, natural gas, agricultural commodities, and global equity indices. In addition to the FOREXTrader Pro platform, FOREX.com also supports the popular MetaTrader (MT4) platform in Arabic, for traders who want to run automated strategies while enjoying the competitive pricing, stability, and service of a global market leader.

FOREX.com's Arabic service is regulated by the UK's Financial Services Authority, which provides clients with a robust regulatory framework and segregated funds protection.

"Traders today want a robust service that operates with strong regulatory oversight," added Mr. Rasoul. "Our FSA regulated service, along with our transparency as a U.S. public company, provides traders with a lot of confidence in choosing FOREX.com as their trading provider. Looking ahead, our goal is to expand our products and services for traders in the Middle East. This includes delivering new, innovative tools, expanding the trading markets we offer and, of course, continuing to provide superior customer service and trading execution."

For more information or to open up a complimentary 30-day practice account, traders should visit www.forex.com or www.forex.com/ar.

*Foreign exchange and CFD trading involves significant risk of loss, and is not suitable for all investors.

About GAIN Capital

GAIN Capital Holdings, Inc. (NYSE:GCAP) is a global provider of online trading services. GAIN's innovative trading technology provides market access and highly automated trade execution services across multiple asset classes, including foreign exchange (forex or FX), contracts for difference (CFDs) and exchange-based products, to a diverse client base of retail and institutional investors.

A pioneer in online forex trading, GAIN Capital operates FOREX.com®, one of the largest and best-known brands in the retail forex industry. GAIN's other businesses include GAIN GTX, a fully independent FX ECN for hedge funds and institutions, and GAIN Securities, Inc. (member FINRA/SIPC) a licensed U.S. broker-dealer.

GAIN Capital and its affiliates have offices in New York City; Bedminster, New Jersey; London; Sydney; Hong Kong; Tokyo; Singapore; Beijing and Seoul.

For company information, visit www.gaincapital.com.

© Press Release 2012

FOREX-Euro falls as minister spotlights Spain funding worry - Reuters

* Euro falls, erasing earlier gains as Spain worries grow

* Spain's Montoro says financial markets shut to Spain

* Market awaits G7 conference call on euro zone crisis

LONDON, June 5 (Reuters) - The euro fell on Tuesday, erasing earlier gains, on growing concerns about whether Spain can restore health to its banks as a minister said high borrowing costs meant Spain was effectively shut out of the bond market.

The comments by Treasury minister Cristobal Montoro highlighted the funding problems facing Spain as investors fretted the country may have to seek external aid.

Analysts said the euro's losses may be limited before an emergency conference call of Group of Seven financial policymakers on the euro zone debt crisis, although the chances of a significant breakthrough looked slim.

The euro fell 0.6 percent on the day against the dollar to hit a session low of $1.2415. It traded more than a cent below an earlier one-week high as investors cut back hefty bets against the currency.

"People will be happy to sell into moves above $1.25," said Anders Soderberg, currency strategist at SEB in Stockholm.

The euro has rebounded from a two-year low of $1.2288 hit on Friday, but Soderberg said its recovery was only "a short-term break in what now seems to be a well-established downtrend".

In addition to the concerns about Spain, investors are worried about the risk that a Greek election in two weeks could push Athens out of the euro.

The depths of the problems facing the euro zone were highlighted by a purchasing managers' survey showing the euro zone's private sector economy shrank in May at the fastest pace in nearly three years.

The common currency faced chart resistance at $1.2545, the 76.4 percent Fibonacci retracement of its decline last week, and at $1.2570, the 23.6 percent retracement of its longer-term decline from a February high near $1.35.

"I don't expect European policymakers to come to an agreement soon. I am ready to sell the euro around $1.2550," said a trader at a Japanese bank in Tokyo.

It also erased earlier gains against the yen and was last down 0.8 percent on the day at 97.08 yen, although this still left it above Friday's 11-year low of 95.59 yen.

Against sterling, the euro was down 0.25 percent at 81.02 pence, off an earlier one-month high of 81.405 pence.

CENTRAL BANK ACTION

The G7 talks prompted some market players to speculate that the European Central Bank could opt for some form of further monetary stimulus when it meets on Wednesday.

International Monetary Fund Managing Director Christine Lagarde said in an interview with a Swedish newspaper that the ECB had room for another interest rate cut.

There has been some talk of a rate cut, although a recent Reuters poll showed only 11 out of 73 analysts polled expected a move this month.

In a sign of increasing concern about the impact of the euro zone debt crisis, the Reserve Bank of Australia cut interest rates by 25 basis points on Tuesday.

The cut was less than some had expected, however, sending the Australian dollar higher. It was last up 0.1 percent against the U.S. dollar at $0.9733, extending its recovery from an eight-month trough of $0.9581 hit on Friday.

However, some see the Aussie trapped in a downtrend as they expect the RBA to cut rates further in coming months.

Traders will also be looking ahead to testimony by U.S. Federal Reserve Chairman Ben Bernanke on Thursday for any hints that Friday's weak U.S. jobs data could prompt a further bout of quantitative easing.

The dollar was down 0.15 percent against the yen at 78.20 yen, taking it closer to Friday's 3 1/2-month low of 77.652 yen though market players were wary about the possibility of Japanese authorities stepping in to stem the yen's rise.

Forex Flash: Today's strategy for EUR/USD – Commerzbank, Danske Bank and UBS - NASDAQ

FXstreet.com (Barcelona) - The three banks have released their trade recommendations for the day. The Copenhagen based bank, Danske Bank, suggests in its daily technical report to "sell at 1.2570 for a 1.2425 objective, stop 1.2628", while Commerzbank recommends to "stand aside for a while." UBS' Chris Walker, believes the cross will be at 1.20 in the next 3 months and at 1.15 in the next twelve months.

The euro continues to be under pressure with news about Germany pressuring Spain to accept a bailout. Also, European indicators have not been doing well: German PMI for services and factory orders came short of expectations, reaching 51.8 and dropping by 3.8% (YoY), respectively. Retail sales in the eurozone had a contraction of 2.5% with respect to the previous year. On the bright side, the services PMI for the eurozone came out above the consensus forecast at 46.7.

The pair is currently trading at 1.2468, losing 0.26%.

Taiwan forex reserves down 1.5 pct in May - CNBC

TAIPEI, June 5 (Reuters) - Taiwan's foreign exchange reserves stood at $389.275 billion at the end of May, down 1.5 percent from the previous month, the central bank said on Tuesday.

Taiwan's reserves are the world's fourth-largest after China, Japan and Russia. The figures do not include gold.

The central bank also said the market value of securities and Taiwan dollar deposits held by foreign investors reached $201.1 billion, equivalent to 52 percent of foreign exchange reserves.

RESERVES M/M CHG FOREIGN HOLDINGS

(US$ bln) (pct) (pct of reserves)

2012

End-May 389.275 -1.47 52

End-April 395.07 +0.31 54

End-March 393.87 -0.14 56

End-February 394.43 +1.06 56

End-January 390.30 +1.25 53

2011

End-December 385.547 -0.62 48

End-November 387.968 -1.36 47

End-October 393.327 +1.00 51

End-September 389.174 -2.78 48

End-Aug 400.294 -0.12 53

End-July 400.76 +0.11 60

End-June 400.33 +0.40 62

End-May 398.683 -0.20 65

End-April 399.54 +1.76 65

End-March 392.63 +0.50 61

End-February 390.69 +0.93 60

End-January 387.111 +1.34 66

(Reporting by Jeanny Kao; Writing by Faith Hung; Editing by Michael Urquhart)

((jonathan.standing@thomsonreuters.com)(+886 2 2500 4881)(Reuters Messaging: jonathan.standing.thomsonreuters.com@thomsonreuters.net))

Keywords: TAIWAN ECONOMY/RESERVES

Eurozone crisis live: G7 finance ministers discuss Europe as Spain pleads for help - as it happened - The Guardian

Time to end the live blog for the day. Here's a closing summary:

• G7 finance ministers and central bankers have discussed the eurocrisis by phone today as fears grow that Europe could trigger a new panic in the global economy. On the call, leaders discussed plans for closer fiscal union across Europe, which increasingly looks like the only way to stem the crisis.

• Spain's prime minister warned that the country is now in a situation of "extreme difficulty". Mariano Rajoy said it was imperative that Europe proves that the euro is irreversable, by agreeing a banking union and embracing eurobonds. Germany, though, remained opposed to allowing Spain's banks to be bailed out without a formal request from the Spanish government.

• A grim set of economic data showed that the eurozone economy is shrinking. Private sector output across the single currency region fell by its fastest rate in almost three years, while retail sales fell 1% and Germany factory orders also dropped. Economists predicted that the eurozone could shrink by 0.5% in the current quarter, putting more pressure on the ECB (which meets to set eurozone interest rates tomorrow).

• With the City closed for business, European stock markets had a mixed session. In quiet trading the French CAC closed 1% higher, the German DAX was broadly unchanged, and the Athens market tumbled by 5%.

We'll be back tomorrow morning. Thanks, and goodnight!

Tomorrow will be interesting - the European Central Bank will hold its monthly rate-setting meeting, Eurostat will announce the second estimate of eurozone GDP for Q1 2012, and traders will return to their desks in the City after a four-day break.

The ECB is expected to leave rates unchanged at 1%, but a shock cut can't be ruled out (especially after the poor economic data this morning).

Speaking of developing economies (see last post), it emerged earlier today that India has drawn up contingency plans for Greece to exit the euro.

"Yes, India does have a contingency plan. There are different crisis management groups within the government to deal with such a possible scenario," Kaushik Basu, the chief economic adviser to finance minister Pranab Mukherjee, told Reuters.He declined to give details of the plan, but another senior official familiar with the planning said the finance ministry and central bank were prepared to take monetary and fiscal measures if necessary to try to insulate India from the shockwaves of a euro zone collapse

One of Barack Obama's top officials has warned this afternoon that the troubles in the eurozone are the biggest threat to the global economy, and that there are already signs of a slowdown in the developing world.

Michael Froman, a senior adviser to the US President, made the comments while attending a panel discussion in Washington. They show that the American government is determined to push for a new push on economic growth at the G20 summit in Mexico in two weeks.

Here are Froman's key quotes (via Reuters):

There's an overwhelming consensus that the focus is on growth, the need for growth (and) the risks to growth around the world...The euro zone crisis is the most significant threat to growth but we see slowing growth in the developing economies.

There was some evidence of this from Vietnam earlier today, where the government warned that the Vietnamese economy might only grow by 5.2% in 2012. While most European countries* would snap your arm off for such GDP expansion, it's actually a downgrade on last month's estimate of 5.6% to 5.8% expansion.

* although not Estonia...

The word from Westminster tonight is that British officials are describing today's G7 teleconference call as a 'stocktaking session', ahead of the upcoming G20 summit.

That backs up Jeremy Cook's point about the big decisions being saved for the Mexico meeting in two week's time (see 5.04pm).

Spanish news wire AGI has a bit more detail of Mariano Rajoy's comments to the Spanish parliament:

Addressing the Spanish Senate, PM Rajoy said the EU has a duty to support financially troubled partners. "Europe must clarify what path it wishes to follow to ensure greater unity; it must clearly state that the euro is an irreversible project and that the euro is not in jeopardy; [Europe] must help nations in need.

So, as indicated earlier (3.59pm) Rajoy is making his bluntest call yet for assistance from the rest of the EU. However, Madrid's reluctance to ask for help itself (rather than simply for its banks) remains a hurdle which neither side can negotiate.

As my colleague Ian Traynor reported earlier (1.47pm), German politicians of all shades are adamant that national banks cannot simply tap the European bailout fund for help.

Someone has to blink - and World First's Jeremy Cook reckons it must be Madrid, telling us by email that:

Spain's banks are like a tinderbox at the moment but their salvation rests in the hands of politicians - a apocalyptic mix of systemic importance and staggering ineptitude. The bank guarantee scheme is a great idea until the Germans get involved and say no; as with most plans for the eurozone at the moment.Although politically destructive and obviously humiliating, it is time for Spain to ask for help from the IMF.

City analysts reckon that the G7 may be keeping its powder dry today, so that world leaders can make a big bang when the G20 meets in Mexico in two weeks time.

Jeremy Cook, chief economist of World First, said this would explain the lack of an official statement after today's teleconference. He told us:

It's not really surprising that the G7 haven't released some form of post-meeting communique; it wasn't expected and the markets have not bothered to ask for one.

The G20 meeting in Mexico in a fortnight could, and probably should, be the place for some sort of announcement as it may be able to counteract any negative news coming from the Greek elections over the weekend.

France's stock market managed a decent recovery today, despite the lack of apparent progress made by the G7. The German market also clawed back its losses, to end almost unchanged.

DAX: down 8 points at 5969, -0.15%

CAC: up 31 points at 2986, +1.07%

The Greek stock market has closed at a new 22-year low, after another day of heavy falls among banking stocks.

The main Athens index closed -5.09%. Traders said the latest selloff was partly due a prediction from Standard & Poor's yesterday that there was a 1 in 3 chance of Greece leaving the euro.

Spain's Mariano Rajoy is speaking in parliament now, and giving the clearest signal yet that Spain needs help.

Rajoy told MPs that Spain is now in a situation of "extreme difficulty", adding that Europe must now 'reinforce' the Euro project – which looks like code for closer fiscal ties, and perhaps the kind of Federal Europe which is now being considered (see today's frontpage story).

The embattled prime minister also told the Madrid parliament that Europe must declare that the euro project is "irreversable".

Rajoy also expressed strong support for a eurozone banking union, and the introduction of eurobonds – two issues which Germany will not accept until closer fiscal is agreed (as confirmed by Wolfgang Schäuble earlier today - see 11.52am)

The US Treasury has just issued its official statement following the teleconference held by G7 finance ministers earlier today.

It's not exactly a hummdinger, but it does reveal that leaders discussed the important issue of closer fiscal ties across Europe.

The G7 Ministers and Governors reviewed developments in the global economy and financial markets and the policy response under consideration, including the progress towards financial and fiscal union in Europe. They agreed to monitor developments closely ahead of the G-20 summit in Los Cabos.

Treasury secretary Timothy Geithner & Federal Reserve chairman Ben Bernanke were both on the call, we believe.

Our Wall Street correspondent Dominic Rushe isn't too impressed, commenting:

The US Treasury is clearly being very cautious and has put out a statement on the G7 meeting that takes bland to a whole new level.

Wall Street has opened for trading, with no real reaction to the news that the G7 teleconference call ended without major fanfare.

The Dow Jones is just 1 points lower at 12100, with the S&P and the Nasdaq both effectively flat. So no relief rally in New York, but no panicky selloff either.

Our Wall Street correspondent, Dominic Rushe, reports:

Yesterday the markets were down 17.11 points, or 0.14%, the fourth consecutive day of losses. Overall the Dow is so far down 479.23 points, or 3.81%, over the four-day period.

But so far it's hardly a Euro-catastrophe. Last week's awful jobs report had the biggest impact on US markets, which seem to be betting that Europe will have to reach some sort of deal. Of course if it doesn't, all bets are off.

There's a sense of anticlimax now that the G7 call has ended, without any clear progress (see 1.53pm)

Investors are growing ever more impatience at Europe's failure to make progress.

Rick Meckler, president of investment firm LibertyView Capital Management in New York, warned that that markets need to see 'concrete plans' soon. He told Reuters that finance ministers can't calm the situation by simply talking:

It has come to a point where the market needs to see some concrete plans....They took comfort in leaders getting together and talking in past times. This time they need to see something definitive to begin to resolve this crisis.

Japan's finance minister Jun Azumi has also caused some concern by telling reporters in Tokyo that the possibility of Greece leaving the eurozone was not discussed (despite the general election being just 12 days away).

What did they talk about, Spanish Banks then? RT @saraeisenFX: G7 didnt discuss Greece leaving the euro: Japan's Azumi

— Robert Passarella (@robpas) June 5, 2012

Breaking news -- the G7 teleconference call has ended.

Disappointingly, there does not appear to be a joint statement (this could change...), but Japan's finance minister Jun Azumi has been discussing the call.

According to newsflashes on the wires, Azumi is explaining that the G7 "agreed to work together to deal with the problems in Spain and Greece". He personally told the call that the current strength of the yen is damaging the Japanese economy, but added that Japan remained its confidence in Europe's response to the crisis.

No mention of 'Germany bashing', though, as one G7 member (not, I think, the UK) was predicting before the call began (see 12.08pm).

Spain's hopes that the eurozone might directly recapitalise its stricken banks without the Rajoy government actually requesting a bailout have been set back by both sides of the political divide in Germany, our Europe editor Ian Traynor flags up from Brussels.

It appears that German politicians remain sticklers for the rules that say only a government can access the bailout kitty, invariably with draconian strings attached.

Ian reports:

The parliamentary leaders of Angela Merkel's Christian Democrats and the opposition Social Democrats are both in Brussels today. They have both urged Mariano Rajoy to hurry up and ask for help while stressing that the rules can't be bent.

Volker Kauder, the CDU's parliamentary leader in Berlin, said there was no point in discussing any other kind of help for Spain.

"Discussions over a new type of aid don't seem very productive in the current situation....The help must be requested by the state concerned, as the rules prescribe. If there is now a debate about the need to recapitalise Spanish banks, the government in Madrid should promptly decide whether it wants access to the EFSF [current temporary eurozone bailout fund]."

Frank-Walter Steinmeier, former German foreign minister and current SPD parliamentary leader, was even stronger in pressing Rajoy to ask for help. "I see a risk that Spain will be too late in deciding to seek protection from the euro rescue umbrella," he said. He was sure that Rajoy would need to request a bailout.

"Spain is in a difficult situation and it's up to Europe to act. The action will be needed very soon....One should try to stabilise the banks conventionally, that is with conditions, via aid to the state."

Referring to Spanish pleas for a direct recapitalisation, supported by France and the European Commission, Steinmeier said: "I am more cautious perhaps than many of the others in this public debate."

John Maynard Keynes, who was born on this date in 1883. Photograph: Topical Press/taken from picture library

John Maynard Keynes, who was born on this date in 1883. Photograph: Topical Press/taken from picture library A quick historical note. Today is the 129th anniversary of the birth of John Maynard Keynes, and the 79th anniversary of the United States coming off the gold standard.

JM Keynes was born on this day in 1883 in Cambridge, going on to reshape economic thinking with his theories of how governments could, and should, use interventionist fiscal policies to regulate the financial cycle and prevent downturns becoming slumps. His theories remain controversial, but advocates argue that Keynesian economics remains our best hope of avoiding another Great Depression (eg, yesterday's interview with Paul Krugman).

Keynes made his reputation during the financial crisis of the 1920s and 1930s, when politicians and central bankers wrestled with the biggest financial panic of the last century. That crisis led to the various leading economies dropping off the Gold Standard as the pillers of the financial system crumbled. America took the plunge on 1933, when Franklin D Roosevelt signed the legislation meant America would no longer peg the dollar to a fixed gold price (although it took until the 1970s for Nixon to finally break the link).

Incidentally, today could also be the anniversary of the birth of ground-breaking political economist Adam Smith (there's some ambiguity about exactly which day he was born in 1723)

Our understanding is that UK chancellor George Osborne is taking part in the G7 call to discuss the eurocrisis.

There's no official word about how the call is going, but an Italian government officials has told the FT that the call is basically a follow-up to the discussion which took place two weeks ago when the G8 met in America.

That suggests that the issues of eurozone bank recapitalisation and growth strategies could dominate the call...

French foreign minister Laurent Fabius has weighed in over the Spanish banking crisis today, telling a conference in Paris that banking union could help address the crisis.

Fabius argued that a solution must be found that does not add to Spain's own debts, at a time when its bond yields are already dangerously high.

Fabius said:

We have to find mechanisms, methods to bring the necessary funds to allow the system to continue to function properly without adding to Spain's budget deficit, otherwise we won't get anywhere....If, to save the bank, you have to increase the deficit and this increase leads to higher interest rates, then it's the snake eating its tail.

He added that France would "favour" a solution based around a banking union.

Of course, Fabius isn't completely impartial here. French banks hold a lot of Spanish debt, and would also benefit from closer banking ties across the eurozone.

So, where are we with Spain? After weeks of deadlock, it does feel as if its banking crisis is close to some kind of resolution.

The key sticking point remains Spain's extreme resistance to taking any form of official bailout. As reported at 12.08pm, that is irking some members of the G7, with Reuters reporting this lunchtime that Madrid's "fatal hubris" is causing some alarm.

The Spanish government does appear to be giving some ground. Treasury minister Cristobal Montoro admitted this morning (see 9.17am) that European institutions need to "open up" and help the country recapitalise its banks.

The hitch, though, is that Europe's bailout funds cannot, as currently defined, pump money into a national banking system directly.

Looking briefly at the currency and commodity markets, the euro has lost more than half a cent against the US dollar this morning. From $1.2490 overnight, the euro has now dropped to $1.242.

The pound is also down against the US dollar, trading around $1.5343.

The strengthening dollar has also pushed down the oil price, with a barrel of Brent crude down 81 cents at $98.04. And the gold price is flat, at $1,618 per ounce.

A source at a G7 country has told Reuters that today's G7 conference call is likely to turn into a "Germany bashing session".

That suggests the US, the UK, France, Italy, Japan and Canada may be taking a united position that Germany needs to change its approach to the crisis.

Reuters' G7 source also says that Germany is "pushing Spain' to take help from the European bailout fund to recapitalise its banks, but that Madrid is currently resisting.

From the terminal:

"They don't want to. They are too proud. It's fatal hubris," the source said of the government in Madrid.

That fits with reports that Spain has been privately pushing for help for its banks without the Spanish state having to take an aid deal. Under the current rules, of course, the European Stability Mechanism cannot directly recapitalise European banks (although many players, including the IMF, think it should able to).

Officially, Germany has been arguing that Spain has been 'everything right'.

German finance minister Wolfgang Schäuble has given an interview to Handelsblatt, in which he reiterates Berlin's position that "a real fiscal union" must be created before more contentious issues such as eurobonds can be considered.

Schäuble told the business daily that closer fiscal ties remain the first step, and even that is a 'medium-term' objective. Banking union could come later, but Schäuble didn't indicate it could happen quickly, saying:

We should take one step after another

There's some more detail here and here.

Schäuble should be on the G7 conference call, starting soon...

An interesting development in the Italian banking sector today – Alessandro Profumo, the former chief executive of UniCredit, has today been indicted in a tax fraud case, according to reports from Milan.

Profumo is one of 20 bankers charged with alleged tax fraud. According to Bloomberg, several other former Unicredit execs are also facing trial, along with some former staff from Barclays. Details here.

The European Union has said that the G7 conference call (due to start in 25mins) will allow the EU to update its partners on the region's response to the ongoing crisis.

At the regular midday briefing, an EU spokesman also explained that the G7 call is part of a "regular exchanges of views", so we shouldn't panic just because finance ministers are talking.

It's not clear, though, which EU officials will be on the call:

EU says cannot yet confirm if EU's Rehn will take part in the G7 call

— Fabrizio Goria (@FGoria) June 5, 2012

City analysts and traders hope that the G7 can make some headway in their conference call at noon BST, but they aren't terribly confident.

Michael Derks, chief strategist of currency trading site FxPro, commented:

Frankly, given the incredibly fragile sentiment evident over recent weeks, the G-7 needs to come up with something fairly convincing to soothe the nerves of traders and investors alike.

A man walks past a board showing graphs of Japan's stock price indexes outside a brokerage in Tokyo, earlier today. Photograph: Toru Hanai/Reuters

A man walks past a board showing graphs of Japan's stock price indexes outside a brokerage in Tokyo, earlier today. Photograph: Toru Hanai/Reuters News of the talks did help push shares higher in Japan overnight, where the Nikkei finished 1% higher. There's less optimism in Europe, though, with German shares lower, and Wall Street expected to open slightly lower (but that could change, depending on how the G7 call goes)

Another piece of poor economic news – German industrial orders fell by 1.9% in April. That is the biggest drop since last November, and worse than expected (economists had predicted -1.1%)

Yet another sign that the eurozone economy has deteriorated in recent months - although the German economy ministry did point out that March had seen surprisingly strong growth, so a fallback in April shouldn't be a shock.

Reuters is reporting that G7 finance minister will hold their conference call to discuss the eurozone crisis at 11am GMT, so in an hour and half's time.

More euro economic gloom -- retail sales across the single currency region fell by 1.0% in April, compared with March. That's the biggest monthly fall since last December.

On a year-on-year basis, retail sales were 2.5% lower than a year ago.

Howard Archer of IHS Global Insight said it was "a dismal day for the Eurozone on the economic front" (with the service sector shrinking at its fastest rate in almost three years).

After an early rally, European stock markets have dropped back, with Germany's DAX in the red again:

DAX: down 54 points at 5923, - 0.9%

CAC: up 7 points at 2962, + 0.26%

IBEX: up 20 points at 6260, + 0.29%

That follows the news that Eurozone private sector shrank again last month (see 9.36am)

Traders work at the stock exchange in Frankfurt yesterday. Photograph: Daniel Roland/AFP/Getty Images

Traders work at the stock exchange in Frankfurt yesterday. Photograph: Daniel Roland/AFP/Getty Images German shares also fall yesterday, on concerns that its exporters will suffer from a global economic slowdown, or worse, if the eurozone crisis is not resolved.

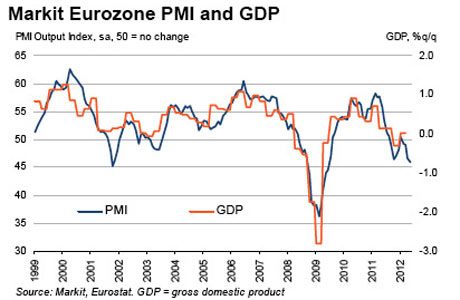

Europe's service sector has suffered its worst monthly decline in almost three years, in the latest evidence that the region's economy is shrinking.

Markit reported its latest PMI data this morning, and the picture across Europe was pretty bleak. Germany's service sector grew at its weakest amount for six months in May, while most other countries' sectors shrank:

Germany: 51.8 (where >50= growth, and <50=contraction)

Spain: 41.8

Italian: 42.8

France: 45.1

When combined with last Friday's manufacturing data (which was also grim), the data shows that the Eurozone's private sector shrank at its fastest pace since June 2009. At 46.0, May's 'composite PMI' was the fourth month in a row to show a contraction. Even Germany's output fell, although at a slower rate than the rest of the eurozone.

Latest economic data shows Europe's economy is shrinking.

Latest economic data shows Europe's economy is shrinking. Chris Williamson, Markit's chief economist, said the data suggests eurozone GDP will fall by as much as 0.5% this quarter (having stagnated in Q1).

There is some convergence among member countries, but unfortunately only in the sense that all of the largest are now experiencing downturns. While Germany is contracting only marginally, alarmingly steep downturns are evident in Spain, Italy and now also France.

Italy seems to be faring the worst, with its PMI consistent with GDP falling by more than 1% in the second quarter.

Spain's Treasury minister has caused some disquiet this morning by stating that the country is effectively shut out of the bond markets -- just two day before it holds a debt sale.

Cristobal Montoro also appeared to signal that Spain needs international help, but not a full bailout, in an interview with Spanish broadcaster Onda Cero.

Montoro told the radio station that:

The risk premium says Spain doesn't have the market door open...The risk premium says that as a state we have a problem in accessing markets, when we need to refinance our debt.

Spain's 'risk premium', measured by the difference between the yield on its 10-year bonds and the German equivalent hit record levels last week. As I type, the spread between the two bond yields is 515 basis points - a massive difference in borrowing costs.

Spain is due to auction €2bn of medium-term debt on Thursday.

Montoro expressed strong support for Europe to create a closer "banking union", saying a decision should be taken at the next EU summit at the end of June. He also argued that "European institutions" should provide funding to help recapitalise its banks, saying Spain needs to show how it will strengthen its banking sector.

That's why it's so important that the European institutions open up and help us achieve, help facilitate, that figure because we're not talking about astronomical figures.

Bloomberg reckons this is the first time a Spanish minister has called for outside funds. Prime minister Mariano Rajoy has long argued that the European Stability Mechanism should be able to recapitalise European banks directly (rather than via the state), without going as far as to state that Spain needs their help.

Montoro also said it was 'technically impossible' to bailout Spain itself – an acknowledgement that Europe's firewall isn't strong enough.

Britain saw its credit rating cut by one notch last night, by ratings agency Egan Jones.

Egan Jones slashed the UK's rating by one notch to AA-minus, from AA, and left a negative outlook on the rating. It warned that Britain may fail to trim its deficit as quickly has planned, saying in a statement that:

The over-riding concern is whether the country will be able to continue to cut its deficit in the face of weaker economic conditions and a possible deterioration in the country's financial sector

Not a very nice way to mark the Queen's Diamond Jubilee...

Egan Jones isn't one of the Big Three rating agencies, and at present it rates many countries as more of a credit risk than Moody's, S&P or Fitch.

Our Europe editor, Ian Traynor, argues in today's Guardian that a "United States of Europe" may be the only way to save the eurozone. Here's a flavour:

The USE – United States of Europe – is back. For the eurozone, at least. Such "political union", surrendering fundamental powers to Brussels, Luxembourg and Strasbourg, has always been several steps too far for the French to consider.

But Berlin is signalling that if it is to carry the can for what it sees as the failures of others there will need to be incremental but major integrationist moves towards a banking, fiscal, and ultimately political union in the eurozone.

It is a divisive and contested notion which Merkel did not always favour. In the heat of the crisis, however, she now appears to see no alternative.

The next three weeks will bring frantic activity to this end as a quartet of senior EU fixers race from capital to capital sounding out the scope of the possible.

As Rainman2 points out in the reader comments, three of Portugal's banks are being recapitalised to the tune of €6.6bn.

The move will mean Banco Commercial Portugues, Banco BPI and Caixa Geral de Depósitos can all hit Europe's tougher capital reserve requirements. The money is coming from Portugal's €78bn bailout (agreed last year, which included €12bn for its financial sector).

Crucially, Portugal is still meeting the terms of its rescue package, despite fears that a second bailout might be needed. Its Troika of lenders announced last night that the Portuguese financial reform programme "remains on track amidst continued challenges." That decision means Lisbon will receive its next tranches of aid, totalling €4.1bn.

The financial markets, though, are still pricing Portugal as a serious risk. It's 10-year bonds are trading at a yield of around 11.5% today, deep into the 'danger zone'.

Canada's finance minister Jim Flaherty. Photograph: Chris Wattie/Reuters

Canada's finance minister Jim Flaherty. Photograph: Chris Wattie/Reuters The news that G7 finance chiefs are to hold a teleconference call today is a clear signal from the world's largest economies that the Eurozone must take rapid steps to stem the crisis.

The call was first revealed by Canadian finance minister Jim Flaherty last night. He told reporters that ministers and central bankers from Canada, the US, Britain, Japan, Germany, France and Italy would hold a special conference call to discuss the eurozone crisis, explaining that:

The real concern right now is Europe of course – the weakness in some of the banks in Europe, the fact they're undercapitalised, the fact the other European countries in the eurozone have not taken sufficient action yet to address those issues of undercapitalisation of banks and building an adequate firewall.

This mesage was reiterated by the US government, with White House press secretary Jay Carney warning that "more steps need to be taken" to address the crisis and reassure the financial markets.

And overnight, Japan's finance minister, Jun Azumi, also confirmed that concerns over the eurozone crisis are now dangerously high, warning:

We have reached a point where we need to have a common understanding about the problems we are facing.

G7 conference calls are usually confidential, so Flaherty's decision to go public may indicate that world leaders are keen to apply the maximum pressure to the eurozone. We don't yet know when the call is taking place.....

Here's a quick agenda of some of the main events and economic data coming up:

• G7 finance ministers hold conference call: timing currently unknown

• Eurozone purchasing manager index on services for May: 9am BST

• Eurozone retail sales for April: 10am BST / 11am CEST

• German factory orders for April: 11am BST/ noon CEST

• Bank of Canada's interest rate decision: 2pm BST/ 9am EDT

Good morning, and welcome back to our rolling coverage of the eurozone financial crisis.

After a day off yesterday to toast her Majesty and put up more bunting, we're back to track the latest action across Europe. The key development this morning is that G7 finance ministers are due to hold emergency talks on the euro zone debt crisis later today. More on this shortly.

Across Europe, pressure is growing on Germany to accept a 'banking union' across Europe. As my colleagues Ian Traynor and Giles Tremlett report:

Europe's leaders appear to be edging towards an ambitious and controversial new blueprint for a federalised eurozone after Paris and Brussels threw their weight behind Spain's pleas for an EU rescue of its beleaguered banks.

At the start of three weeks likely to be crucial to the survival of the euro, the new French government and the European commission voiced strong backing for a new eurozone "banking union" to save the single currency.

The plan could see vast national debt and banking liabilities pooled – and then backed by the financial strength of Germany – in return for eurozone governments surrendering sovereignty over their budgets and fiscal policies to a central eurozone authority.

A "gang of four" – the European council president, the commission chief, the president of the European Central Bank and the head of the eurogroup of 17 finance ministers – has been charged with drafting the proposals for a deeper eurozone fiscal union, to be presented to an EU summit at the end of the month.

Things may be quieter than normal, with the UK enjoying another bank holiday today. But other European markets will be trading as usual, after a mixed day yesterday, so there should be plenty to report. There's also some interesting economic data due, covering the world's service sectors, eurozone retail sale, and German factory orders.

MAS underlines key challenges for Islamic finance to continue thriving - theborneopost.com

[getrss.in: unable to retrieve full-text content]

SINGAPORE: Monetary Authority of Singapore (MAS) managing director Ravi Menon has underlined key challenges for Islamic Finance to continue thriving. “Islamic finance has come a long way. “As it embarks on its next phase of growth, the industry must ...

No comments:

Post a Comment